Analytics cookies

We use Microsoft Clarity on public pages to understand clicks, scrolling and page performance. Accept analytics cookies to help us improve the site, or reject to continue without analytics cookies.

Privacy policy

Discovering that spray foam may affect your mortgage, sale or roof can feel overwhelming. A clear review starts by understanding the issue, preparing the documents, and deciding which complaint or support route may be worth considering.

Complete the short form below for a free initial review of your circumstances, supporting documents and possible next steps.

Mortgage issues

Organise lender, broker, valuation and survey comments where spray foam affects lending.

Evidence review

Bring together sales paperwork, product documents, photos, reports and complaint replies.

Financial loss

Separate documented costs from general dissatisfaction before choosing the next route.

Complaint support

Prepare clearer complaint material and escalation packs where the evidence supports it.

Common problems

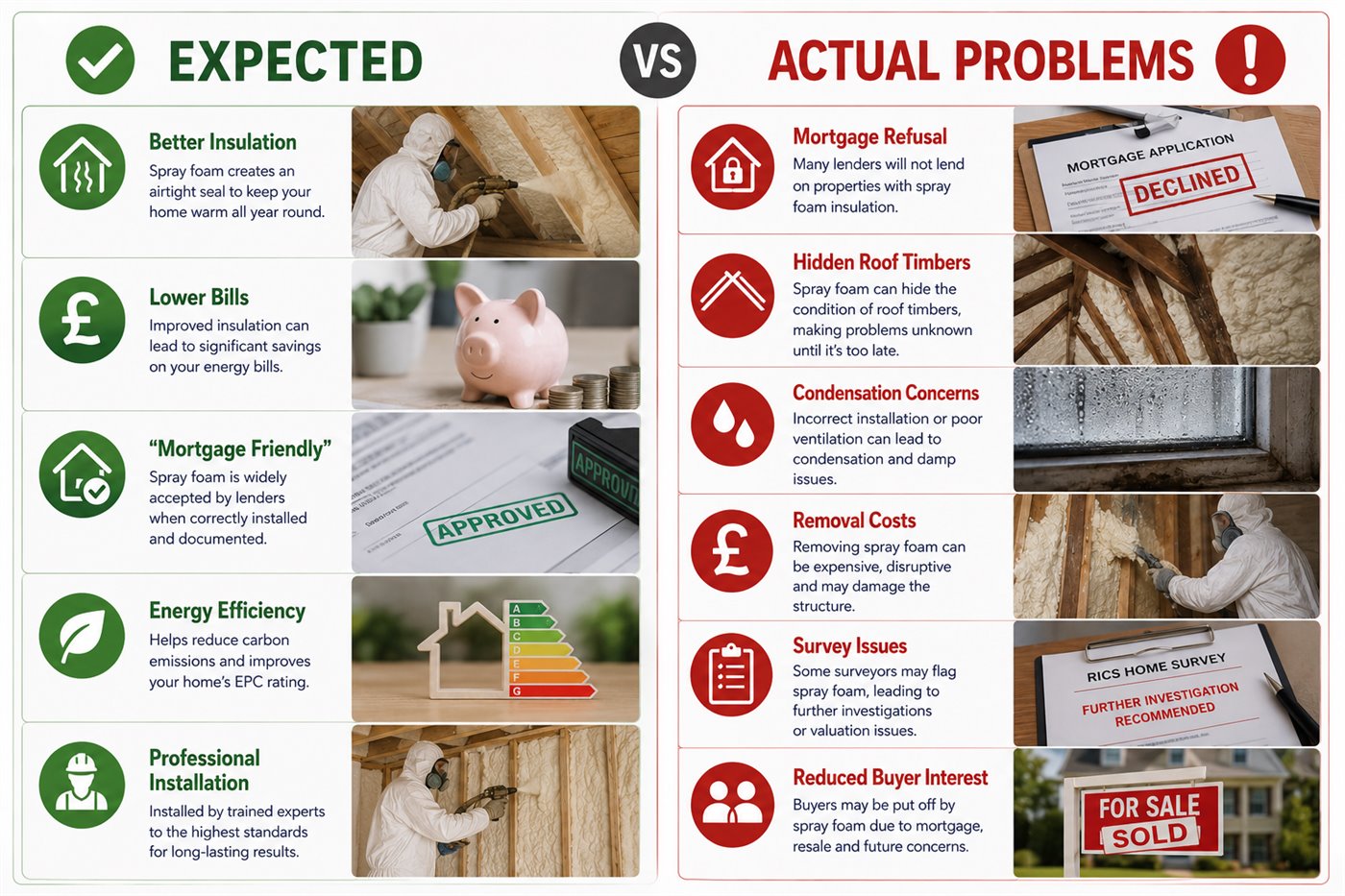

Many homeowners only discover the issue when a sale, remortgage, equity release application or survey creates a practical problem. These are the main concerns Quaerens sees in spray foam enquiries.

Review lender, valuer and broker comments where a mortgage or remortgage has been refused, delayed or restricted.

spray foam mortgage refusalCheck whether spray foam has affected an equity release valuation, lender condition or application route.

equity release concernsUnderstand why buyers, surveyors or lenders may raise questions before a sale can complete.

spray foam sale concernsCollect evidence about ventilation, condensation, damp, timber condition and how the foam was installed.

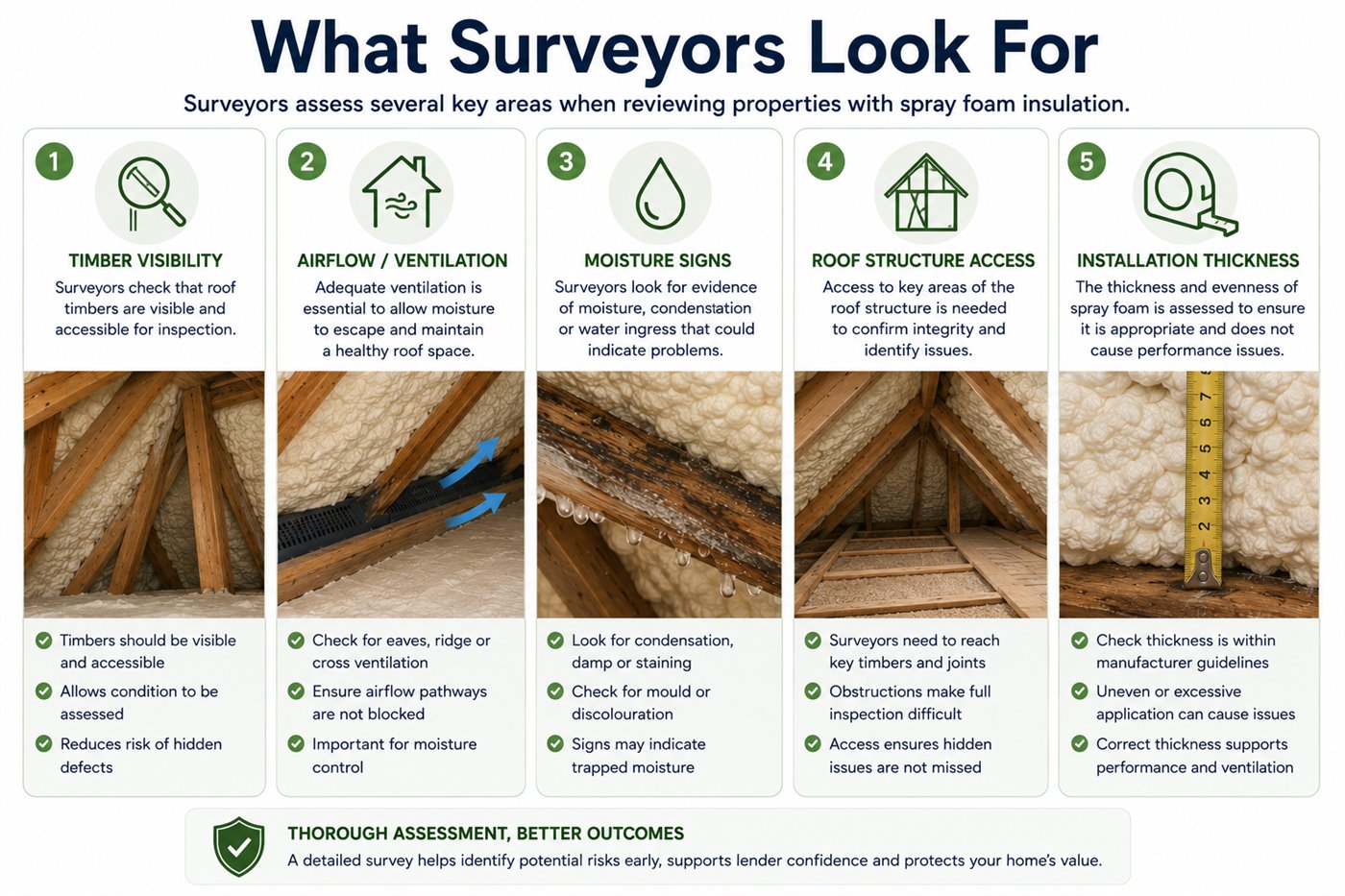

surveyor concern evidenceLearn why restricted inspection of rafters, timbers, felt or membranes can matter to valuers and lenders.

why lenders worryOrganise removal quotes, roof repair comments, scaffolding costs and replacement insulation estimates.

spray foam removal costsCheck whether finance, credit card or linked payment evidence may point to a separate complaint route.

finance and Section 75 routesConnect spray foam evidence with wider property, survey, repair and contractor dispute support.

property disputes hub

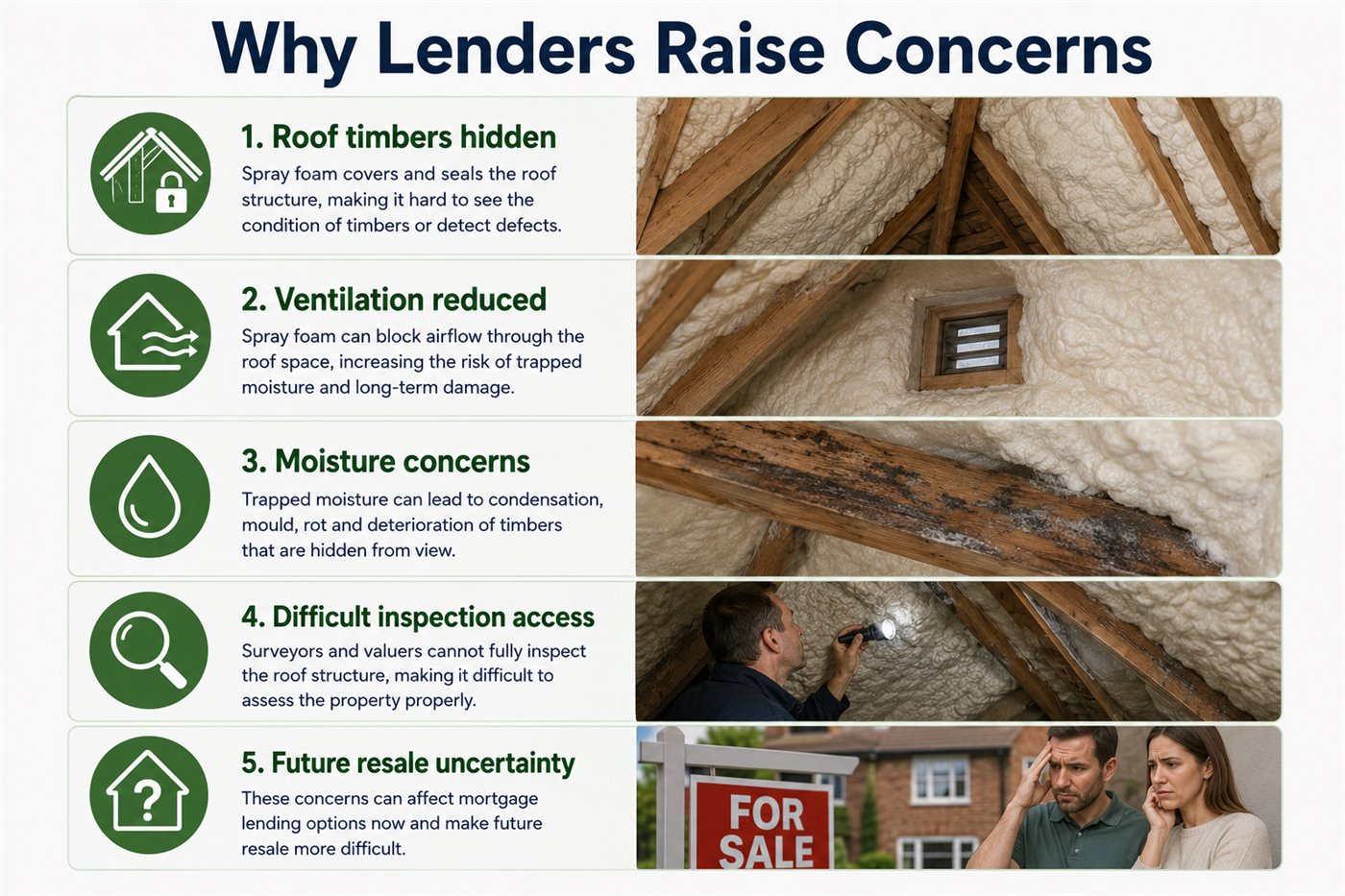

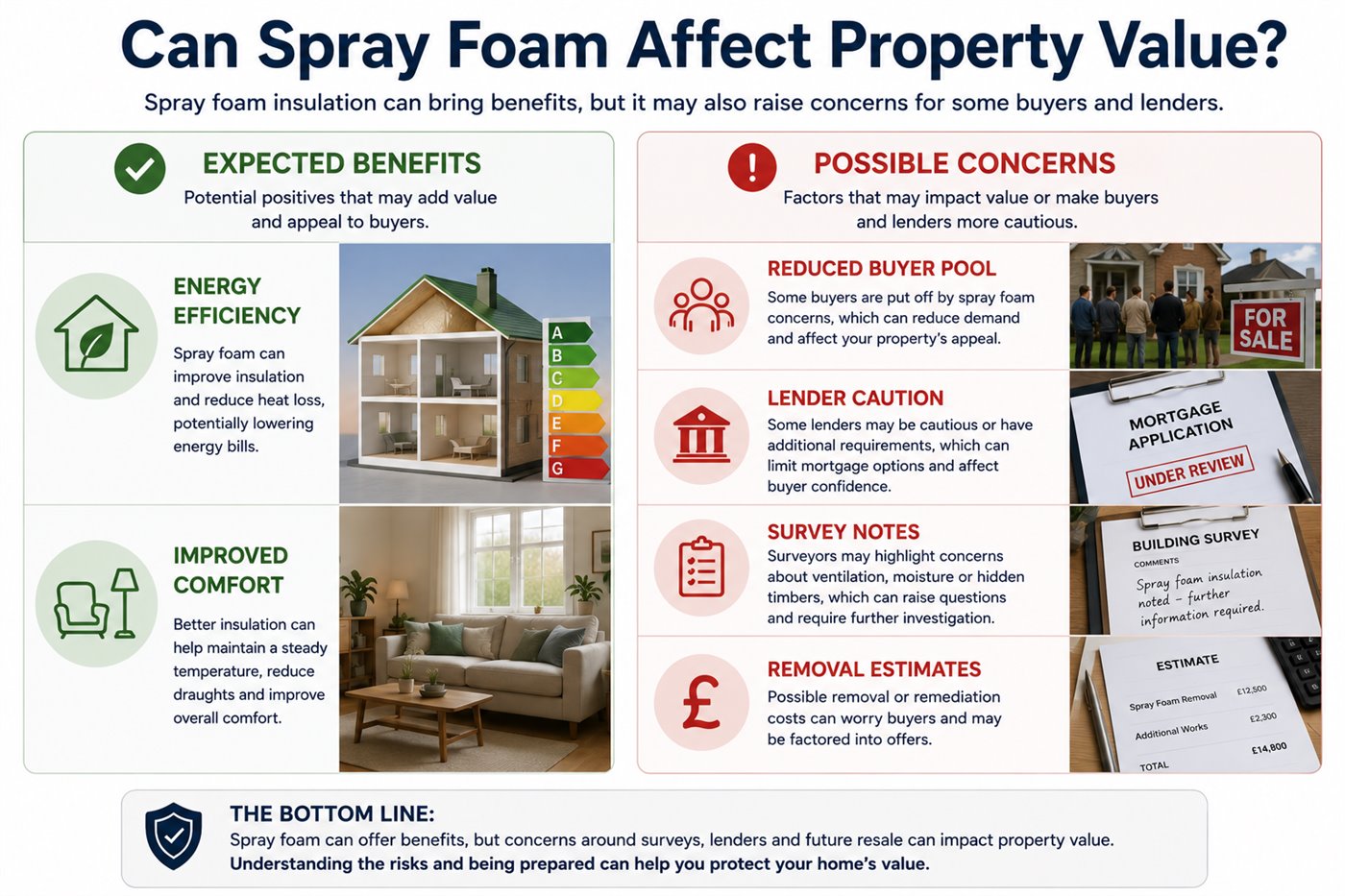

Lender and valuer policies vary. One lender may ask for documents, another may require inspection evidence, and another may decide not to proceed. Requirements can also change over time, so the most useful evidence is the written response on your property.

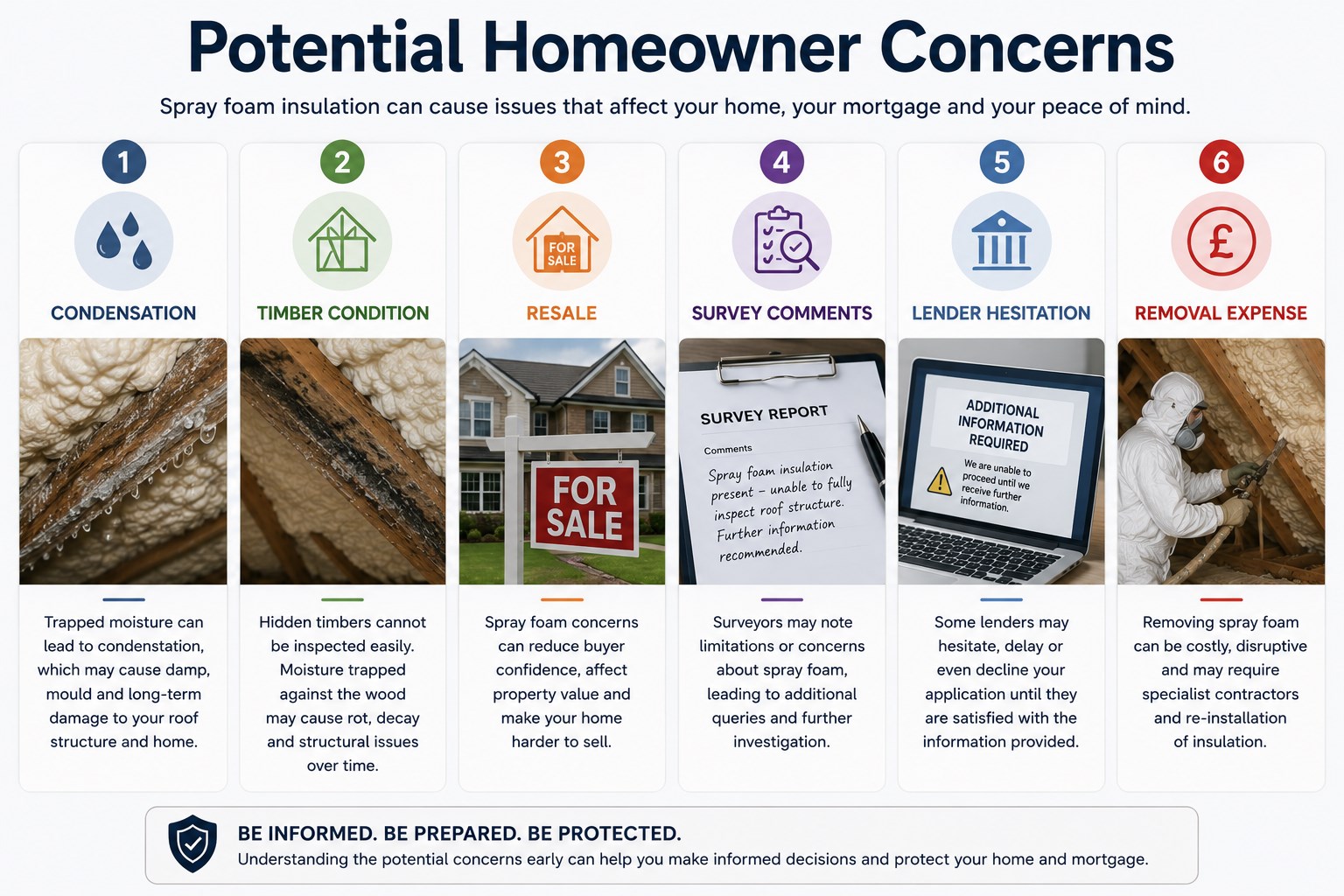

If foam covers rafters, felt or junctions, a surveyor may be unable to comment confidently on timber condition or hidden defects.

Questions can arise about airflow, ventilation routes, trapped moisture, roof membrane condition and signs of damp.

Guarantees, product sheets, installer paperwork and certificates can help, but certification alone does not guarantee mortgage acceptance.

Different products can raise different practical questions about density, vapour movement, inspection and removal difficulty.

Some cases may require a suitably qualified surveyor, roofing professional or other relevant expert. Quaerens cannot determine whether a lender will approve a mortgage, but we can help organise the evidence and possible complaint route.

The product label is only one part of the review. Installation method, roof type, ventilation, paperwork, photographs and the actual lender or surveyor comments all matter.

Open-cell foam is generally less dense and more flexible. The review may consider where it was applied, whether ventilation was preserved and whether timbers remain inspectable.

Closed-cell foam is generally denser and can be harder to remove. The review may consider whether it restricts inspection or raises concerns about moisture movement.

Foam applied directly to felt, membranes or timbers can create different concerns from foam installed with clear ventilation and proper records.

Product certification may be useful evidence, but it may not answer every lender, valuer or buyer concern about a specific property.

Removal-cost searches are common because quotes can vary substantially. A careful review should look at why removal is being recommended, what work is included and whether the cost links to the original sale, installation or finance route.

Loft size, foam thickness, open-cell or closed-cell product, access, waste removal and labour time can all affect the quote.

Some projects may require difficult access, protection measures, scaffolding or roof covering disturbance.

Quotes may change if timber, felt, membrane, damp or ventilation problems become visible only after foam is removed.

Making good, replacement insulation, certification or inspection after works may add to the documented cost.

Important removal-cost note

Quaerens does not publish a single fixed average removal cost because the evidence varies from property to property. Removal quotes should be treated as case-specific and supported by photographs, inspection notes and scope of works.

The financial impact of a spray foam dispute depends on the evidence, payment method, complaint route and circumstances. The table below shows examples of costs that may be relevant and the documents usually needed to support them.

| Possible financial loss | Supporting evidence |

|---|---|

| Installation price | Contract, invoice, quote, product paperwork, survey or guarantee documents. |

| Finance interest and charges | Finance agreement, statements, settlement figures and payment correspondence. |

| Survey and valuation costs | Survey invoice, valuation report, lender comments or broker correspondence. |

| Removal costs | Removal quotation, scope of works, contractor notes, photographs and access requirements. |

| Roof repair or replacement costs | Surveyor or roofer report, repair quote, inspection photographs and technical comments. |

| Failed sale or reduced property value | Estate agent correspondence, buyer withdrawal, reduced offer, valuation notes or sale chronology. |

| Higher borrowing or remortgage costs | Mortgage offer, refusal, broker emails, rate comparison or product evidence. |

| Other documented consequential losses | Receipts, correspondence and a chronology showing how the cost links to the spray foam issue. |

Important

Not every cost will be recoverable. The purpose of the preliminary assessment is to distinguish documented financial loss from general dissatisfaction and to identify which complaint routes may be relevant.

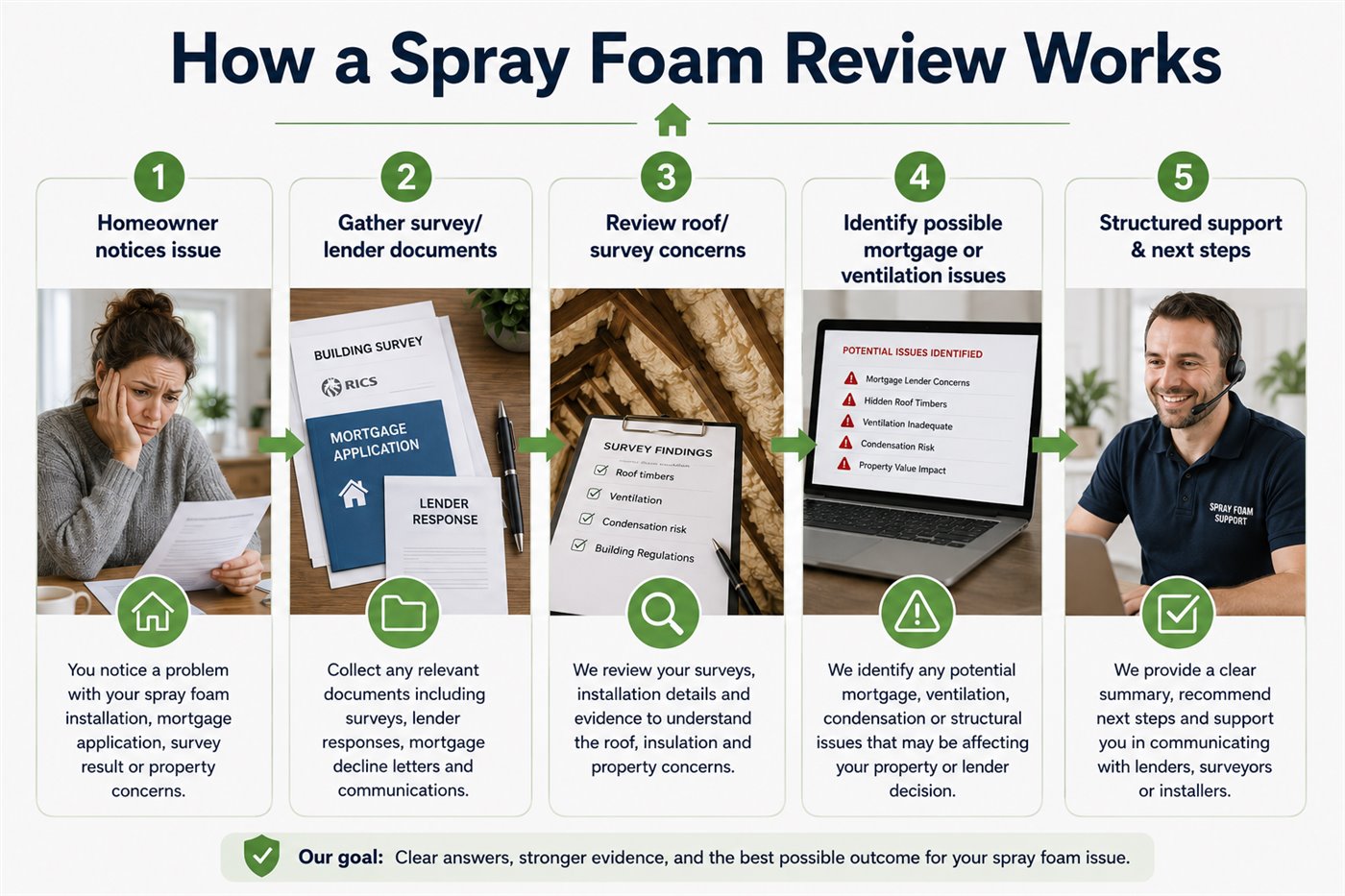

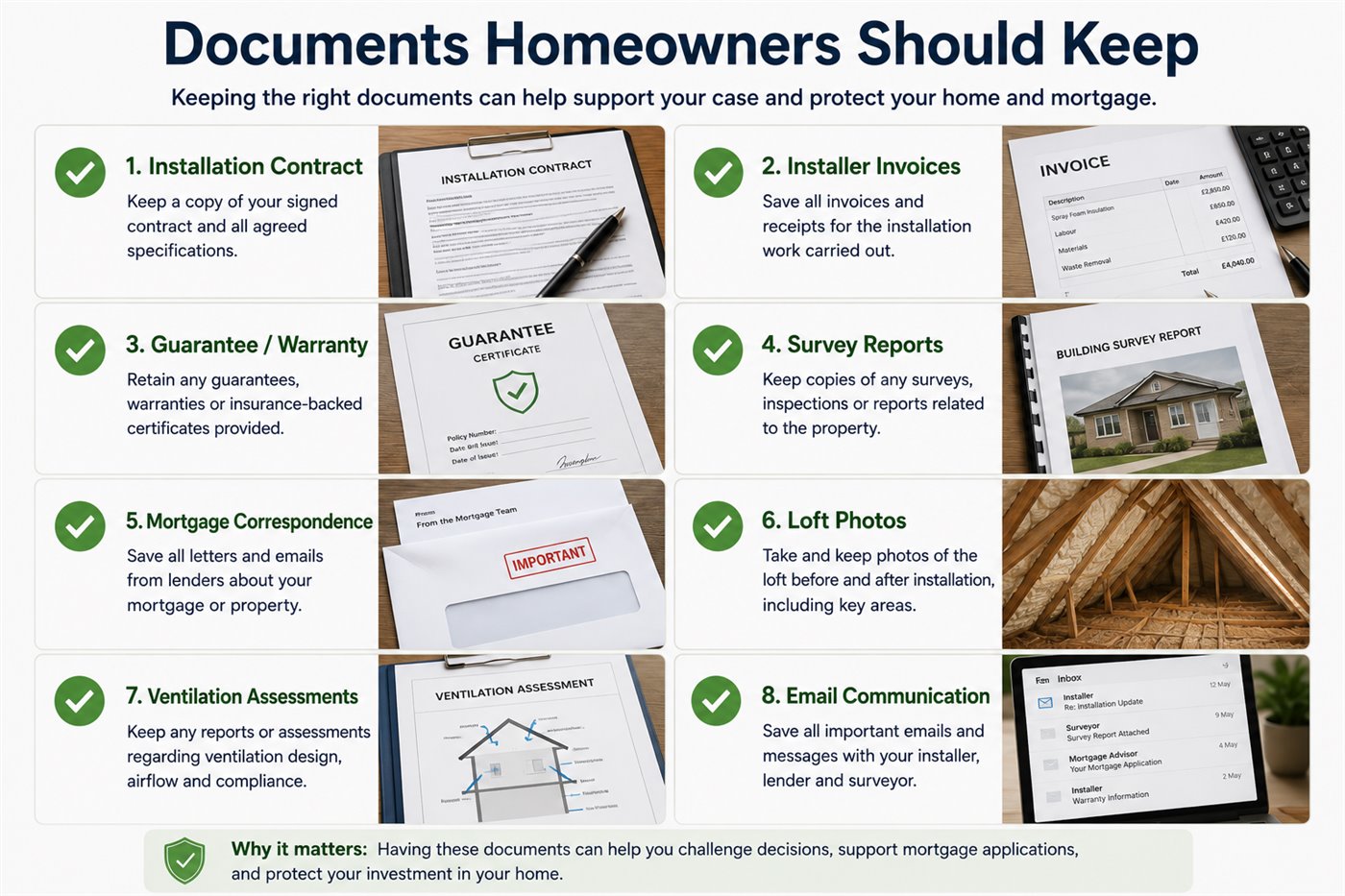

A stronger review usually starts with a clear file. Gather whatever you have and do not worry if some documents are missing; gaps can be identified during the assessment.

We look at the issue affecting your mortgage, sale, survey, finance, installation or removal position.

We review the paperwork you provide and identify missing documents that could help clarify the route.

We organise what happened, when it happened, what was promised and when the problem was discovered.

We identify apparent sales representations, installation concerns and documented financial loss.

We consider possible routes involving the installer, finance provider, card provider, warranty route or escalation body.

Where appropriate, we help organise complaint wording, evidence bundles and escalation material.

Where technical inspection, litigation or regulated financial advice may be required, the client may need to instruct an appropriately qualified professional. Quaerens focuses on practical document, evidence and complaint support.

We review the information you provide.

We contact you to discuss your circumstances.

We explain what additional documents, if any, may be helpful.

We outline any appropriate complaint or support route based on the information available.

These anonymised examples show the type of fact pattern that may be reviewed. They do not describe guaranteed outcomes.

A homeowner preparing to sell received survey comments about restricted timber visibility and lender concern. The evidence reviewed included the installation invoice, product documents, survey notes, buyer correspondence and removal quotation. The assessment focused on what was said at sale, whether risks were explained and what financial loss was documented.

A homeowner paid for spray foam through finance after being told it would improve the property. Later, a remortgage route became difficult and removal quotes were obtained. The review considered the finance paperwork, sales representations, lender comments, roof photographs and whether a finance-provider complaint route might be relevant.

The route depends on who sold the product, how it was paid for, what paperwork exists and what problem has now arisen.

Review sales claims, suitability discussions, guarantees, paperwork and risk warnings.

mis-sold spray foam supportWhere payment was made by finance or credit card, separate complaint routes may need assessment.

Section 75 supportUse clearer wording, chronology and evidence references when raising or escalating a complaint.

stronger complaint preparationBring together quotes, roof notes, photographs and making-good costs before relying on removal figures.

removal-cost evidence guidance

Where Quaerens has a legitimate factual page, we link to it neutrally. A named company page does not mean every customer has a valid complaint.

Common evidence patterns where the issue arises during a mortgage, remortgage or sale.

spray foam mortgage refusal supportPages focused on removal quotes, reinstatement and the documents that help explain costs.

spray foam removal cost supportPages focused on surveyor concerns, roof inspection and property-sale evidence.

spray foam survey problem supportThese references can help homeowners understand the wider context. They do not decide the outcome of any individual complaint.

Request your free initial assessment

Send a short summary of the spray foam issue, what has happened with your mortgage, sale, survey, finance or removal quote, and what documents you already have.

Before the form

Final check

If spray foam is affecting your mortgage, sale, survey, finance or removal costs, request a free initial assessment and find out what evidence matters most.

Request My Free Spray Foam Review